Meta Description: Discover how ACA subsidies and healthcare subsidy changes in 2026 affect your premiums after enhanced Obamacare subsidies expired. Check 2026 income limits and eligibility now. (152 characters)

URL Slug Suggestion: aca-subsidies-2026-changes-income-limits

TL;DR / Key Takeaways

- Enhanced ACA subsidies expired at the end of 2025, leading to higher out-of-pocket premiums for millions in 2026 and the return of the “subsidy cliff” at 400% FPL.

- Premium tax credits remain available for households earning 100–400% of the Federal Poverty Level (FPL), with required contributions up to 9.96% of income.

- Major impact: Average subsidized premiums could more than double, potentially pushing some to drop coverage—up to millions uninsured without action.

- Act now: Use Healthcare.gov tools to estimate your subsidy, explore state options, and plan for income changes.

- 2026 trends: Rising premiums, policy debates in Congress, and potential extensions highlight the need for proactive health insurance shopping.

Quick Answer

ACA subsidies (premium tax credits) in 2026 help lower monthly premiums for Marketplace plans if your household income is 100–400% of the Federal Poverty Level. Enhanced subsidies from the Inflation Reduction Act expired at the end of 2025, causing higher costs and reintroducing the subsidy cliff above 400% FPL (e.g., ~$62,600 for a single person). Use Healthcare.gov to estimate eligibility and savings. (58 words)

Understanding ACA Subsidies in 2026: The Big Shift After Enhanced Support Ends

The Affordable Care Act (ACA), often called Obamacare, has provided healthcare subsidies since 2014 to make Marketplace insurance more affordable. These ACA subsidies include premium tax credits (reducing monthly payments) and cost-sharing reductions (lowering deductibles/copays).

In 2026, a major change hit: the enhanced subsidies—expanded under the American Rescue Plan (2021) and extended by the Inflation Reduction Act (2022)—expired December 31, 2025. Millions now face higher premiums, with the “subsidy cliff” returning for incomes over 400% FPL.

This post breaks down ACA subsidies 2026, income eligibility, impacts, and strategies to stay covered affordably.

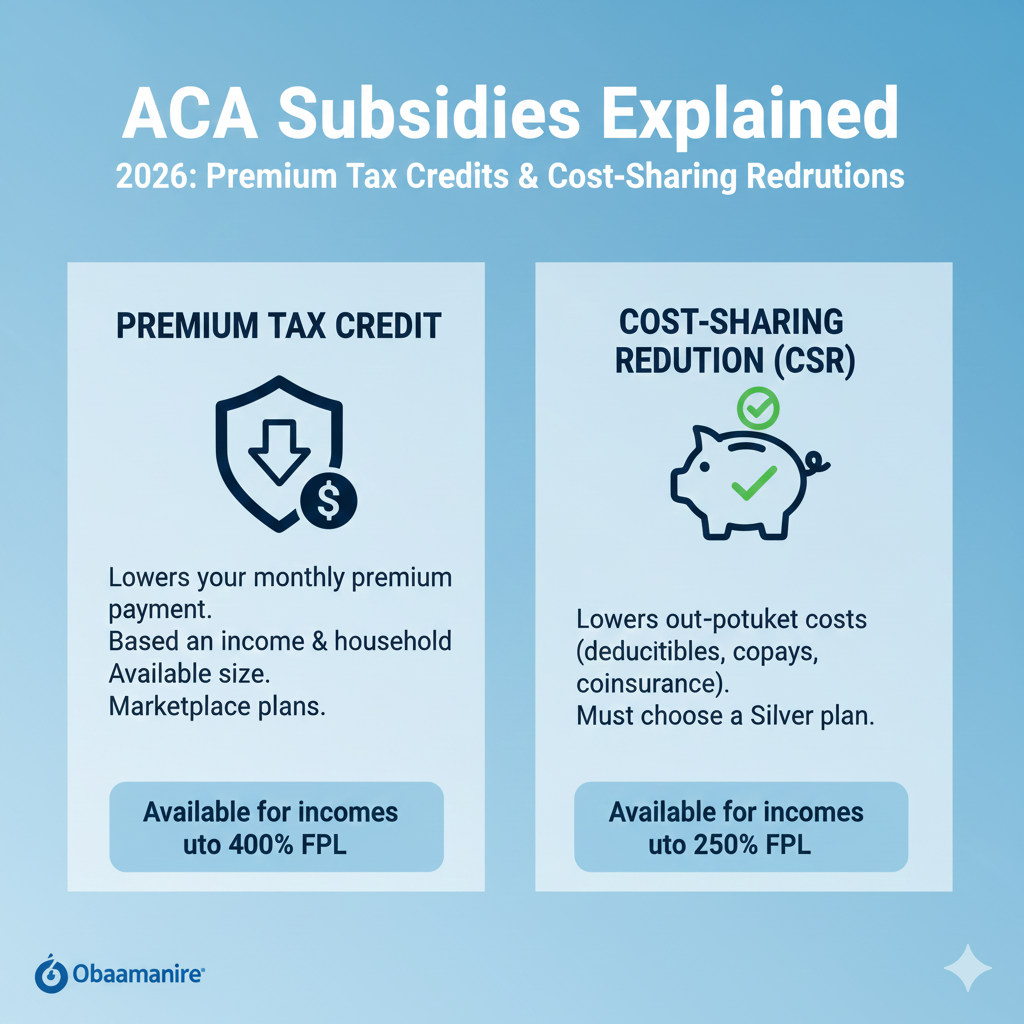

What Are ACA Subsidies and How Do They Work?

ACA subsidies (or healthcare subsidies) are financial aids via the Health Insurance Marketplace (Healthcare.gov or state exchanges).

Two main types:

- Premium Tax Credits (PTCs): Advance payments reduce monthly premiums.

- Cost-Sharing Reductions (CSRs): Extra savings on out-of-pocket costs for Silver plans (incomes 100–250% FPL).

Eligibility uses Modified Adjusted Gross Income (MAGI) and household size. Subsidies are based on the benchmark Silver plan.

2026 Healthcare Subsidy Income Limits: The Return of the 400% Cliff

For 2026 coverage (based on 2025 FPL guidelines), ACA subsidy income limits cap at 400% FPL. No subsidies above this—unlike 2021–2025.

Example 2026 thresholds (continental U.S.):

- Single person: 400% FPL ≈ $62,600

- Family of 4: ≈ $128,600

Required household contribution for benchmark plan:

- 100–133% FPL: ~2.10%

- Up to 200% FPL: ~6.60%

- 300–400% FPL: ~9.96%

- Above 400%: Ineligible (subsidy cliff returns)

Table: 2026 ACA Subsidy Income Limits (Select Household Sizes)

| Household Size | 100% FPL | 200% FPL | 400% FPL (Subsidy Cutoff) |

|---|---|---|---|

| 1 Person | $15,650 | $31,300 | $62,600 |

| 2 People | $21,150 | $42,300 | $84,600 |

| 4 People | $32,150 | $64,300 | $128,600 |

(Source: Federal guidelines; varies slightly by state/territory)

Common Mistakes to Avoid:

- Using last year’s income instead of estimated 2026 MAGI.

- Ignoring household changes (e.g., adding a dependent).

- Not reporting income changes mid-year, leading to repayment at tax time.

- Assuming subsidies apply to all plans—benchmark Silver determines amount.

(link to related post about how to estimate your MAGI for ACA subsidies)

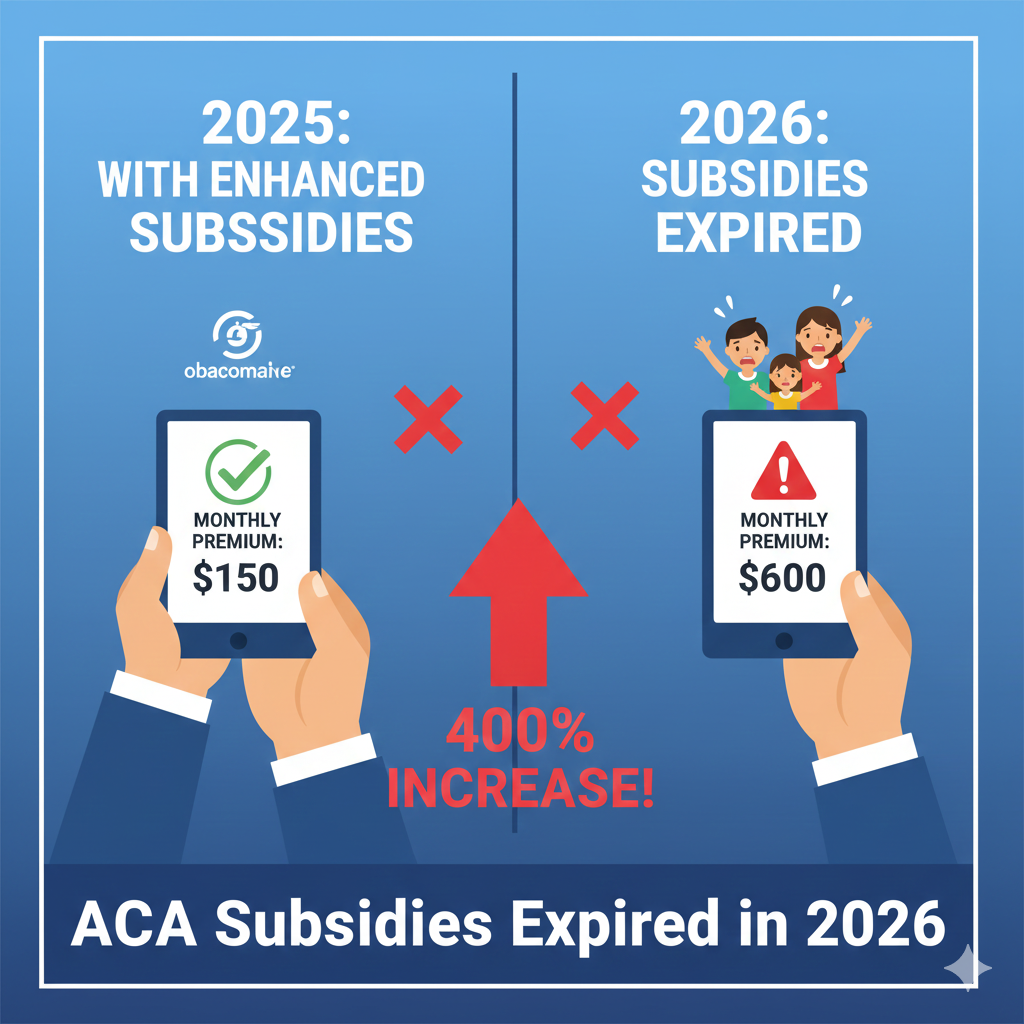

How the Expiration of Enhanced ACA Subsidies Changes Everything in 2026

From 2021–2025, enhanced subsidies capped contributions at 8.5% of income (even above 400% FPL) and boosted amounts significantly. Enrollment doubled, premiums dropped for many.

Now in 2026:

- Premiums for subsidized enrollees could rise 114% on average (from ~$888 to $1,904 annually).

- Millions may lose eligibility or drop coverage due to costs.

- “Subsidy cliff” discourages earning more—$1 over the limit can mean thousands in extra premiums.

Pro Insights for 2026 Trends:

- Rising premiums: Insurers cite drug costs, utilization, and subsidy uncertainty—median increases ~18% for 2026.

- Congressional action? House passed a 3-year extension bill in early 2026, but Senate fate is uncertain—bipartisan talks ongoing.

- State variations: Some states (e.g., CA, NY) offer additional subsidies to cushion impacts.

- Tools: Use updated KFF or Healthcare.gov calculators for 2026 estimates.

Actionable Tips: How to Qualify and Maximize Your Healthcare Subsidy in 2026

Step-by-Step Solutions to Secure Affordable Coverage:

- Estimate income: Use Healthcare.gov’s income calculator for accurate 2026 MAGI.

- Apply/update application: Visit Healthcare.gov during Open Enrollment (typically Nov–Jan) or Special Enrollment.

- Choose wisely: Pick Silver plans for CSRs if eligible (100–250% FPL).

- Report changes promptly: Update income/family size to avoid tax repayment surprises.

- Explore alternatives: Check Medicaid eligibility or state subsidies.

- Plan ahead: If near the cliff, consider deductions or income timing.

Tips:

- Shop early—premiums rise with uncertainty.

- Consider HSAs if eligible (new 2026 rules expand Catastrophic plan options).

- Consult a certified Marketplace navigator for free help.

Read More

Remembering Ahn Sung-ki in 2026: Why the Nation’s Actor Still Inspires a New Generation

Common Mistakes That Cost You Money on ACA Government Subsidies

- Overestimating income → missing subsidies.

- Underestimating → large tax repayment.

- Ignoring CSRs → higher out-of-pocket costs.

- Delaying enrollment → missing deadlines.

- Not comparing plans → leaving money on the table.

FAQs

What are ACA subsidies in 2026?

ACA subsidies are premium tax credits and cost-sharing reductions for Marketplace plans. In 2026, standard subsidies apply (100–400% FPL), after enhanced versions expired.

Do healthcare subsidies still exist in 2026?

Yes, but less generous. Premium tax credits are available up to 400% FPL; no eligibility above that.

What is the income limit for healthcare subsidy 2026?

400% of FPL (e.g., $62,600 single, $128,600 family of 4). Exceeding this creates the subsidy cliff.

How much are Obamacare subsidies in 2026?

Varies by income, age, location. Average subsidized premiums rose significantly post-expiration—use calculators for estimates.

Can I qualify for healthcare subsidy if over 400% FPL in 2026?

No, unless Congress extends enhanced rules. The cliff returns.

What happens if enhanced ACA subsidies don’t come back?

Premiums could double for many; millions risk losing coverage. Some states provide extra help.

How do I estimate my ACA subsidy for 2026?

Use Healthcare.gov tools or KFF calculator with your projected income, household, and ZIP code.

Will Congress extend ACA subsidies in 2026?

Debates continue—House advanced a bill, but Senate outcome uncertain. Monitor news for updates.

Stay informed on ACA subsidies changes—sign up for our newsletter for monthly updates on healthcare policy, subsidy calculators, and tips to save on insurance. Your health coverage matters—let’s keep it affordable together!